funding your own disruption

How Kodak and Netflix faced the exact same strategic crossroad, and took opposite paths to the future

In 1975, a 23-year-old Kodak engineer named Steve Sasson walked into a room full of executives holding something that looked like a toaster with a lens bolted on. He took a photo. He pulled a cassette tape out of the side. He played it back on a TV screen.

Nobody asked how it worked.

They asked why anyone would want to take a picture that way when there was nothing wrong with film.

Thirty-two years later, a small, profitable DVD-by-mail company faced the same choice Kodak had faced. Its own core business was working. Its own core business was still growing. And it still had to decide whether to pivot away from the thing that was working, toward something smaller and unproven.

That company was Netflix. In 2007, DVD-by-mail was not a dying business looking for a lifeline. It was a healthy, growing subscription business with no external crisis forcing any change. Netflix pivoted away from it anyway.

It was the same fork in the road. It was the same slow-moving disruption. Two profitable, dominant businesses each stared at a smaller, uncertain thing nibbling at the edges of their own Cash Cow, and each one had to decide whether to pivot toward it.

Kodak refused to pivot in time. Netflix did.

This is the fork I want to look at.

The Framework

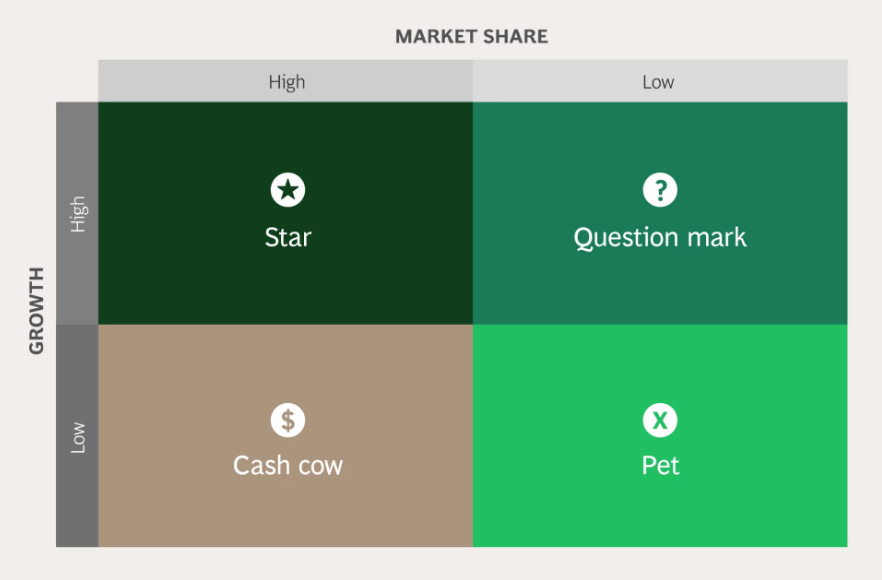

There is a tool from the 1970s that explains exactly why these two stories split the way they did. It is called the BCG Growth Share Matrix, and Boston Consulting Group built it to answer one question: where should this business get its next dollar, and where should it stop getting any? It plots every business along two lines. One line measures how fast the market around it is growing. The other measures how much of that market it actually controls.

Every business lands in one of four quadrants once you plot it this way.

A business with low growth and high share is a Cash Cow. It is mature and it is profitable, and BCG’s own guidance is simple. Milk it for cash, and reinvest that cash elsewhere.

A business with high growth and high share is a Star. It has real future potential, and the guidance here is just as direct. Invest in it significantly, because it is already winning and still growing.

A business with high growth and low share is a Question Mark. It is unproven, and BCG’s guidance is the most honest of the four. Invest in it or discard it, depending on its actual chances of becoming a Star. Nobody gets to skip that judgment call.

A business with low growth and low share is what BCG itself calls a Pet, the quadrant everyone else just calls a Dog. The guidance is blunt. Liquidate it, divest it, or reposition it.

The matrix comes with an instruction. You are supposed to take the cash your Cows generate and pour it into your Question Marks, before you have to, not after. It is uncomfortable, because it means spending your most reliable business’s money on something that has not proven itself yet. But it is the only way a Question Mark ever gets enough runway to become a Star before somebody else’s does.

Kodak had a Cash Cow, and it had a Question Mark sitting right next to it. Netflix had the exact same setup, decades later. Only one of them actually followed the instruction.

Kodak: Defending the Cow

Here’s what makes Kodak’s story so much worse than the version you’ve probably heard. It’s not a story about a company that failed to see the future. Kodak saw it with unusual precision.

In 1979, a Kodak employee named Larry Matteson wrote an internal report predicting the complete shift to digital photography would happen by 2010. He was off by a few years. The transformation was largely complete by the early 2000s.

In 1981, Kodak’s own market intelligence team ran a study asking whether digital photography could eventually replace film. The conclusion carried both bad news and good news. The bad news was yes, eventually it could. The good news was that Kodak had roughly a ten-year runway to prepare before it became a real threat.

Ten years of runway. An internal prediction accurate to within a year of the real thing. And the invention itself, sitting in-house since 1975, patented and shelved.

Kodak had every input a company could ask for. What it did with all of it was defend the Cow.

In fact, Kodak made exactly the mistake that George Eastman, its own founder, had avoided twice before. Eastman gave up a profitable dry-plate business to move to film when film was still the uncertain bet. He invested in color film even though it was demonstrably inferior to the black-and-white film Kodak already dominated. Both times, he chose the harder, unproven path over the comfortable one. Kodak’s leadership in the 1980s had his own company’s history sitting right in front of them, and made the opposite call.

Film wasn’t just profitable. It was Kodak’s entire operating identity, a business that dominated a mature, slow-growth category and had for decades. Digital was the Question Mark. It was unproven, it was capital-hungry, and worst of all from the inside, it was aimed directly at the thing that paid everyone’s salary. So instead of funding the Question Mark while there was still time, Kodak spent the decade defending the Cash Cow and looking for growth somewhere else entirely.

In 1988, that meant buying a pharmaceutical company, Sterling Drug, for $5.1 billion, on the theory that Kodak was really a chemical business at heart. Kodak later sold it off in pieces for roughly half of what it paid. Chemically treated photo paper, it turned out, has very little in common with cardiovascular drugs.

In 1989, Kodak’s board had a real chance to change course. Colby Chandler, the CEO, was retiring, and the choice for his successor came down to two men. Kay R. Whitmore had spent three decades climbing the ranks of the traditional film business. Phil Samper had a genuine appreciation for where digital technology was headed. The board picked Whitmore.

The New York Times covered the decision at the time, and the quote says everything you need to know about which way Kodak had just chosen to go.

“Mr. Whitmore said he would make sure Kodak stayed closer to its core businesses in film and photographic chemicals.”

When Kodak did eventually release digital products, they weren’t bets on the future. They were built to protect the past. The Advantix Preview was a digital camera that still required you to buy film and pay for prints. It flopped, because nobody could figure out why they would pay for digital convenience and film costs in the same purchase. As late as 2007, Kodak was still running marketing campaigns insisting Kodak was back on digital, three decades after Sasson’s original demo, in the same year a completely different company was making its own decision about its own Question Mark.

The ending writes itself from there. Kodak’s Cash Cow never got a Star to replace it. It just curdled, in place, into a Dog. The company filed for bankruptcy in 2012, the same year Sasson’s original digital camera patent had already sat expired for five years, mismanaged by the one company that had actually built it.

Netflix: Feeding the Question Mark

Reed Hastings, Netflix’s co-founder, had been describing a world where entertainment arrived over the internet years before Netflix had streamed a single frame of anything, and before the infrastructure even existed to support it. Even the company’s own name reflected that bet. Netflix built “net” into its identity before it had anything running on the internet at all.

By 2007, Netflix’s DVD-by-mail business was a genuine Cash Cow in every sense the matrix intends. It was dominant, profitable, and still growing, with around 7 million subscribers and nearly a decade of customer data behind it. There was no external crisis forcing a change, no Wired cover declaring Netflix dead, and no moment where the company sat 90 days from bankruptcy the way Apple once had.

That is what makes the decision to launch streaming that year genuinely harder than Kodak’s. Kodak was staring at a slow-moving iceberg with a decade of warning and still didn’t turn the ship. Netflix turned the ship while the current business was still working, which meant giving up short-term comfort for a bet nobody was asking it to make.

The belief behind that decision had been sitting there for over a decade before Netflix ever acted on it. Hastings described this future as early as 1999, in a conversation with Ted Sarandos, who would go on to become Netflix’s own co-CEO. He told Sarandos that almost all entertainment would eventually arrive into the home over the internet, at a time when literally none of it did.

Hastings was also, according to reporting on his thinking at the time, determined not to let anyone do to Netflix what Netflix had already done to Blockbuster. Having watched one dominant incumbent get disrupted, he treated disruption as inevitable, and decided Netflix should be the one to disrupt itself rather than wait for someone else to do it first. So the company made a conscious choice not to defend the business that was working. As DVD growth started to slow, Netflix simply invested more into streaming, on the theory that this was where the future was headed, not because the old business had already failed.

The commitment to that bet went further than most companies would tolerate. Ted Sarandos described just how far in a 2024 interview. At the point where the DVD business was driving all of Netflix’s profit and a large share of its revenue, the company made a deliberate call. As Sarandos put it, “we made a conscious decision to stop inviting the DVD employees to the company meeting.” It is the opposite of what Kodak did when it picked Whitmore, a company deciding on purpose to stop listening to the voice of its own Cash Cow, on the theory that the old business would otherwise talk the new one out of existing.

The Stumble

In September 2011, Hastings announced that Netflix would split entirely in two. Streaming would stay under the Netflix name. DVD-by-mail would spin off into a separate company called Qwikster, with its own website, its own account, and its own billing.

The backlash was immediate and brutal. Subscribers did not want two logins and two websites for one habit. Coming right after a July price increase that had already split the bundled subscription price by as much as 60 percent, the Qwikster announcement landed like a second insult. Netflix lost 800,000 subscribers that quarter. The stock fell by more than 75 percent over the following months, by Hastings's own account.

Twenty-three days later, Hastings killed it. Years afterward, in a 2020 interview, he did not soften what happened. He called it the biggest mistake in the company’s history, and put the blame squarely on himself.

“I made a major error in splitting the DVD and streaming services and increasing the pricing in 2011, called Qwikster. The stock went down 75% over four or five months. It was a big error. And we lost subscribers, etc. And certainly I took ownership of it...”

Here is why Qwikster belongs in this story rather than getting cut as a footnote. It is the mirror image of Kodak's mistake. Kodak's failure was protecting its Cash Cow so completely that its Question Mark never got fed. Netflix's failure, for those 23 days, was trying to cut its Cash Cow loose too fast and too carelessly, underestimating how much the DVD business still mattered.

By the following quarter, DVD subscribers still made up nearly 40 percent of Netflix's total subscriber base, not just a financial fact but a competitive one, since splitting the businesses would have let Apple and Blockbuster compete against each half of Netflix separately instead of facing the bundle at once.

Netflix’s real institutional skill turned out not to be the 2007 call by itself. It was building a repeatable habit of making that same call again. Streaming matured from Question Mark into Star, and then into the new Cash Cow, the one that funded the next Question Mark, original content, starting with House of Cards in 2013. Kodak ran the cycle once and got it wrong. Netflix has now run it at least twice and mostly gotten it right, Qwikster included.

The Key Takeaway

Here's the part of this story that's easy to miss because it hides behind the more dramatic details. Kodak's failure looks like a failure of vision, but Kodak actually saw the future with unusual precision. Its own report named the year. Its own scientist held the patent. So the real lesson has to be something else, since vision was clearly present all along.

The missing ingredient was the willingness to make a bet before it was forced, using money that everyone in the room could see was working perfectly well right now. That's a much harder thing to ask of an organization than simply understanding a trend. Understanding a trend costs nothing and asks nothing of anyone. Funding a Question Mark means telling the people responsible for this quarter's results that some of their budget is going to a project with no track record yet. Netflix found a way to do exactly that, early enough that the bet was still cheap.

That's the real asymmetry between these two companies, and it comes down to timing more than intelligence. Netflix launched streaming while DVD was still healthy, so if streaming had struggled, the company could have absorbed it and adjusted. Kodak waited until digital had already become the market, so by the time it acted, the cost of being wrong had already compounded for decades. Every year of delay raised the price of the eventual reckoning, until the whole bill came due at once, in a bankruptcy filing.

Which is also why Qwikster matters more than it might first appear to. Netflix moved boldly on the big bet and overreached on a smaller one, and the difference in outcome came down to how quickly each decision got tested against reality. Kodak's decades of delay meant its mistake sat untested until it became unrecoverable. Netflix's three weeks of overreach ran straight into furious subscribers almost immediately, which is exactly what made the mistake cheap and fast to fix.

So the real question worth asking is simpler than "do we see the disruption coming." Most companies do, eventually, the way Kodak did in 1975 and again in 1979 and again in 1981. The sharper question is whether you're willing to spend money on that disruption while it's still affordable to be wrong, and whether your organization is built to find out quickly when it's made a mistake.

References

How Steve Sasson Invented the Digital Camera

Netflix’s Streaming Pivot Included a Surprisingly Harsh Decision